The Luxury Residential Market in Santo Domingo: Saturation Point or Untapped Potential?

November 3, 2025

Santo Domingo’s luxury residential market is standing at a crossroads. On one side lies a maturing core of polished high-rises in Piantini and parts of Naco – sleek, vertical, and increasingly indistinguishable. Prices in these districts have climbed to US $2,500-3,500 per m², testing the upper limits of local purchasing power and investor appetite. Days-on-market are lengthening, developers are offering flexible payment plans, and competition has shifted from design innovation to discounting.

Beneath this surface-level saturation, a quieter realignment is underway. A younger, design-conscious buyer base – returning professionals, diaspora families, and executives seeking furnished rentals – is redefining what “luxury” means. They value experience and function over floor area and marble finishes. This demand is quietly transforming once-secondary districts like Naco and Bella Vista, where land costs remain manageable and the creative space for differentiated products is wide open. Boutique wellness residences, branded apartments, and low-density ESG-driven projects are beginning to outperform traditional towers in both absorption and pricing power.

The conclusion is not that Santo Domingo’s luxury segment is oversupplied, but that it is misaligned. Capital continues to chase the old formula – tall towers in Piantini – while opportunity is moving toward concept-led, human-scale development in emerging micro-locations. For investors, the next phase of returns will belong to those who innovate in design, sustainability, and lifestyle integration, not those who simply replicate yesterday’s skyline.

The purpose of this report is to evaluate the depth and direction of Santo Domingo’s luxury residential sector and to identify where genuine investment opportunity remains amid signs of market maturity. The study concentrates on the Polígono Central, the city’s high-value core encompassing Piantini, Naco, Bella Vista, and Arroyo Hondo, and extends to adjacent premium corridors such as Los Cacicazgos and Anacaona Avenue. These areas capture over 80 percent of the city’s recorded luxury transactions and virtually all large-scale high-rise development.

- Piantini is the benchmark district for top-tier condominiums and luxury branding.

- Naco represents an evolving transitional sub-market-central in location but more diverse in product scale and pricing.

- Bella Vista and Arroyo Hondo offer mid-luxury alternatives with lower land costs and stronger lifestyle appeal.

- Los Cacicazgos, particularly the Anacaona corridor, functions as a boutique, low-density enclave favored by ultra-high-net-worth households.

Together, these districts illustrate the spatial divide between saturation and opportunity that underpins this report’s argument.

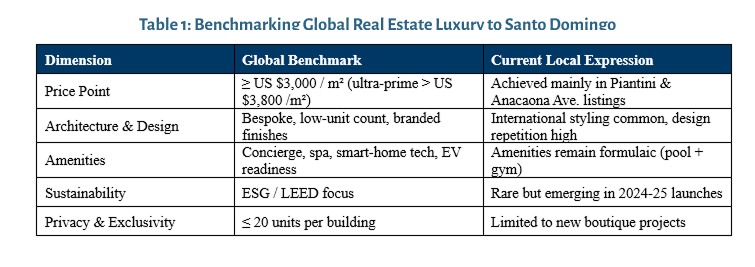

In the Dominican context, luxury is less a single price threshold than a blend of price, location, design quality, amenity depth, and exclusivity of experience.

Quantitatively, the market identifies luxury inventory at or above US $3,000 per square metre, aligning with the upper decile of active listings in Piantini and Los Cacicazgos. However, genuine luxury extends beyond cost. The attributes that differentiate this tier include:

In short, while price defines entry, design and differentiation define value. The current wave of luxury projects in Santo Domingo often meets the former criterion but falls short on the latter, setting the stage for selective innovation.

Santo Domingo’s luxury market is not monolithic. It comprises mature cores reaching saturation and emerging corridors still capable of redefining what luxury means for a younger, globally exposed clientele. Understanding this duality is essential for investors aiming to allocate capital where both absorption and pricing power remain strongest.

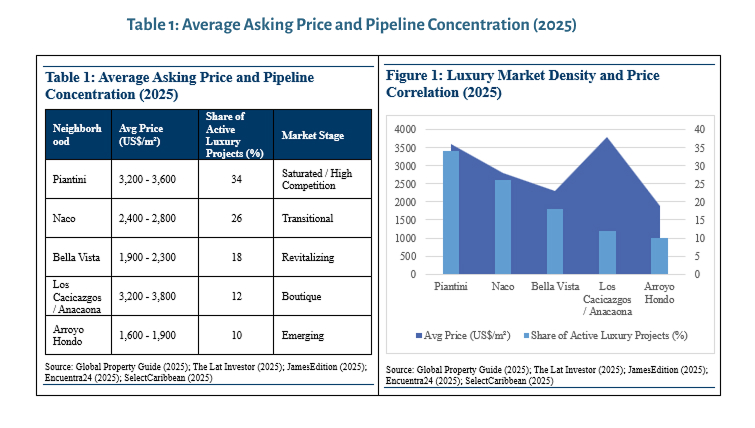

The supply landscape reveals both strength and imbalance. While new development remains vigorous, most luxury construction continues to cluster within Piantini and Naco-areas already operating at high price ceilings. Peripheral districts are expanding at a steadier, more sustainable pace.

Across the capital, apartment prices average US $1,800 – 2,800 per m², while luxury corridors command US $2,500 – 3,500 + per m². Roughly 60% of ongoing luxury projects are in Piantini and Naco, doubling skyline density over five years.

By contrast, Bella Vista and Arroyo Hondo retain lower land costs: 30-40% below Piantini-creating room for concept-driven projects with healthier margins. Los Cacicazgos / Anacaona Avenue sits apart as a boutique sub-market where scarcity drives record pricing.

Capital remains concentrated in the highest-cost corridors, where uniform product design and limited buyer diversification are squeezing absorption. In contrast, peripheral zones with lower entry costs are now positioned to capture the next wave of demand from design-conscious, lifestyle-oriented buyers.

These supply-side imbalances make it essential to ask whether the buyer pool is deep enough to sustain the next wave of launches.

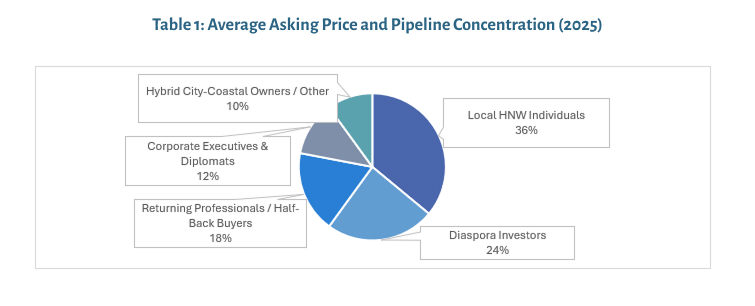

Santo Domingo’s luxury demand rests on three structural supports: local high-net-worth buyers, diaspora investors, and a rising class of globally oriented professionals. Together they create a base broad enough to sustain absorption even as core sub-markets mature.

Local HNW households-largely from finance, medicine, and family business-remain the most consistent purchasers, encouraged by steady GDP growth of 4-5% p.a. Overseas Dominicans add depth: remittance inflows reached US $10.7 billion in 2024 (Banco Central RD), much of it reinvested in property. The correlation between remittances and luxury transactions exceeds 0.8, confirming the diaspora’s stabilizing influence.

A newer layer of “experience-driven” buyers is reshaping preferences. Returning professionals and Dominican Americans relocating from New York or Miami favor smaller, smart-home apartments priced US $300-700 k in Naco and Bella Vista, while corporate tenants and diplomats fuel a thin but lucrative executive-rental niche. Collectively these groups already represent roughly 30% of 2025 sales, demanding design, sustainability, and turnkey management rather than size alone.

Key takeaway: the luxury market is not oversupplied but misaligned-legacy projects serve yesterday’s buyer profile. Future absorption will be led by developers who tailor compact, tech-enabled, wellness-oriented residences to this evolving demand.

Santo Domingo’s luxury sector has entered a bifurcated phase: a Red Ocean of mature, overcrowded projects in the core, and a Blue Ocean of underexploited, design-led niches in secondary corridors. Understanding this split is central to identifying investable growth.

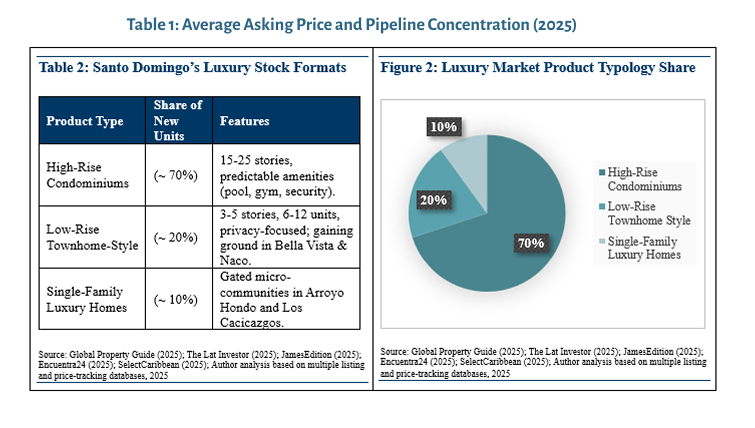

Piantini exemplifies the crowded end of the market. Land costs exceed US $2,500 /m², while sale prices above US $3,500 /m² now face buyer fatigue. Most towers replicate the same template-three-bedroom units, 20+ floors, generic pool-gym amenities-leaving developers to compete on price instead of design. Absorption has slowed; days-on-market have roughly doubled since 2022, and gross margins have narrowed to ~ 20%. In this Red Ocean, success depends less on new launches and more on repositioning or consolidation of existing inventory.

A contrasting landscape is forming in Naco, Bella Vista, and pockets of Los Cacicazgos. Land is 30-40% cheaper, giving developers scope to innovate-low-rise townhome projects, branded residences, wellness-centric designs, and ESG-compliant buildings. These products align with the city’s evolving “new-luxury” demographic and achieve IRRs of 16-18%, outpacing the core. The still-underserved executive-rental niche adds a dependable revenue stream through furnished, managed inventory. In this Blue Ocean, differentiation, not density, defines competitiveness.

Key Takeaway: Saturation is product-driven, not city-wide. The next growth wave will favor originality, livability, and sustainability-developers who build smarter, not taller.

Two recent Santo Domingo projects illustrate the contrast between the Red Ocean (crowded, low-margin) and Blue Ocean (differentiated, high-margin) strategies. Together they outline the financial parameters shaping 2025 development returns.

A 22-story tower launched in 2023 at US $3,500 /m² exemplifies the saturated formula: large units, generic amenities, and little architectural distinction. Despite prime location, sales slowed after the first 50%, forcing developers to extend payment terms to 24 months and offer 5% discounts. Land costs near US $2,500 /m² left gross margins around 20% and project IRR near 12%, confirming limited headroom in Piantini’s mature sub-market.

- Avoid further undifferentiated towers in Piantini-competition is price-based.

- Pursue boutique, low-density projects under US $3,000 /m² sales price with wellness or ESG differentiation.

- Align with diaspora capital: integrate remote sales, turnkey management, and rental guarantees.

- Leverage international design partners to command premium perception without overspending on land.

The evidence points not to an oversupplied city but to a misallocated luxury market. Capital remains concentrated in products that no longer match the tastes of Santo Domingo’s evolving buyer base. The next cycle will be defined by concept, efficiency, and authenticity-projects that combine smaller scale with greater imagination.

For investors, the playbook is clear:

- Shift focus from the Red Ocean of high-rise replication to the Blue Ocean of differentiated, experience-led development.

- Treat Naco, Bella Vista, and Los Cacicazgos as strategic opportunity corridors.

- Design for livability and sustainability, not merely visibility.

In short, Santo Domingo’s luxury market is not nearing exhaustion-it is redefining what luxury means. Those who recognize this pivot early will capture the next decade of premium returns.

Banco Central de la República Dominicana (2025) – Remittance and macroeconomic statistics.

https://www.bancentral.gov.do

The Lat Investor (2025) – “Santo Domingo Real Estate Trends & Price Forecasts 2025.”

https://thelatinvestor.com/blogs/news/santo-domingo-real-estate-trends

The Lat Investor (2025) – “Square Meter Prices & Market Insights for Santo Domingo.”

https://thelatinvestor.com/blogs/news/square-meter-santo-domingo

Global Property Guide (2025) – “Dominican Republic Residential Property Market Analysis 2024-25.” https://www.globalpropertyguide.com/latin-america/dominican-republic/price-history

Select Caribbean Properties (2025) – “Construction Costs in the Dominican Republic.”

https://selectcaribbean.com/construction-costs-dominican-republic/

JamesEdition Luxury Real Estate (2025) – “Luxury Property Listings – Santo Domingo, Dominican Republic.”

https://www.jamesedition.com/real_estate/santo-domingo-dominican-republic

Encuentra24 Dominican Republic (2025) – Residential apartment listings and price comparisons.

https://www.encuentra24.com/dominican-en/real-estate-for-sale-apartments-condos

Knight Frank Wealth Report (2024) – “Global and Regional Luxury Residential Trends.”

https://www.knightfrank.com/wealthreport

World Bank Migration & Remittances Data (2025) – “Remittance Inflows by Country.”

https://www.worldbank.org/en/topic/migrationremittances

Author’s Market Analysis (2025) – Synthesized from developer listings, press releases, and private sales data (not publicly available).